Are you underusing Account Aggregator?

Kinjal Bhatt

Marketing Specialist

|

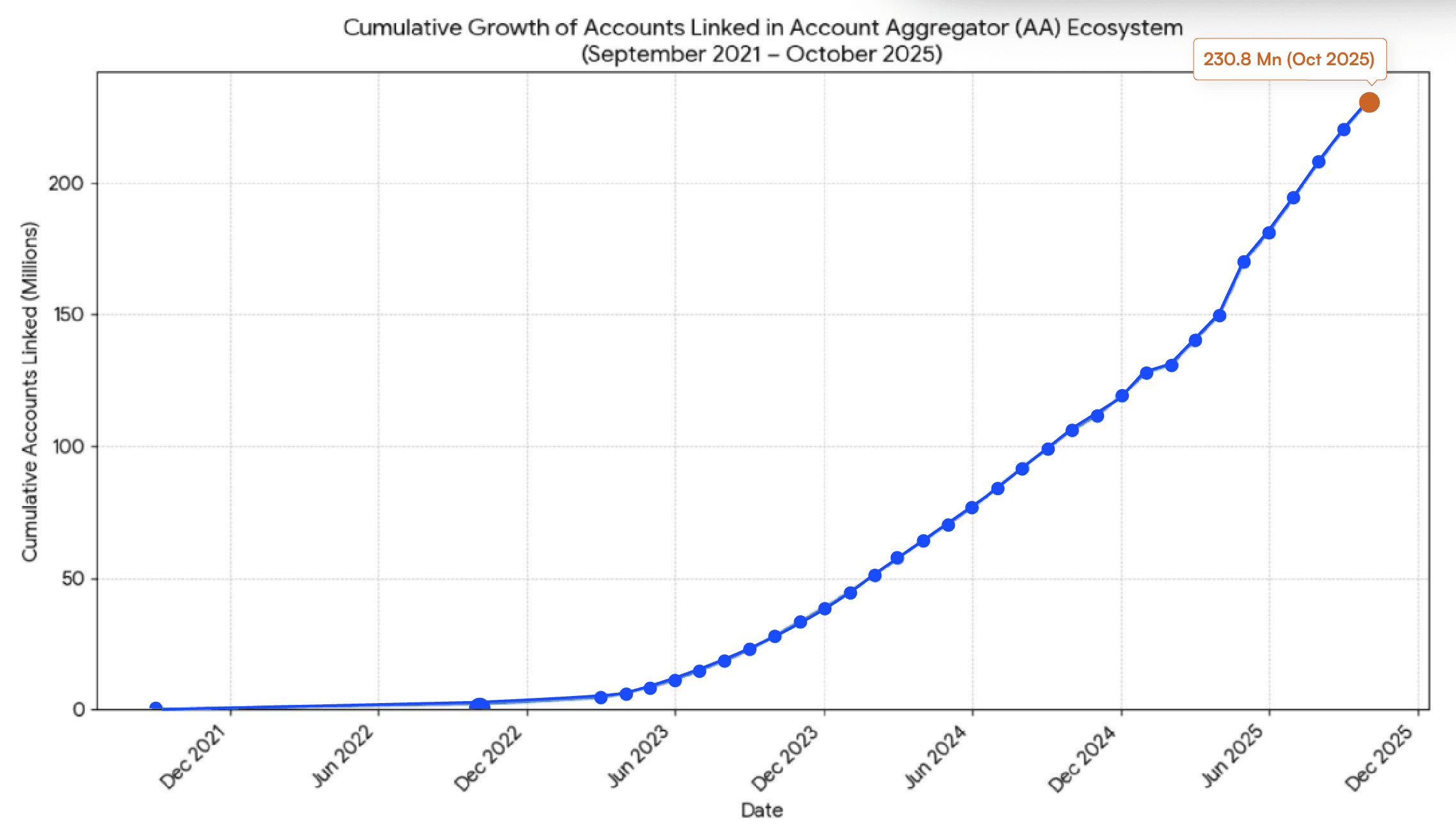

Account Aggregator (AA) has undoubtably revolutionized loan underwriting by offering faster credit assessments, enhanced fraud detection, and borrower-preferred journeys. This graph further elaborates the significance and speed of AA adoption.

Data source: Sahamati & pib

However, despite being operational for four years, AA’s success largely remains confined to loan underwriting use case.

Lenders who limit AA to this stage alone miss out on substantial opportunities to improve loan monitoring, collections, and risk management which can substantially reduce delinquencies and increase portfolio health.

Beyond underwriting: Unlocking more value from AA data

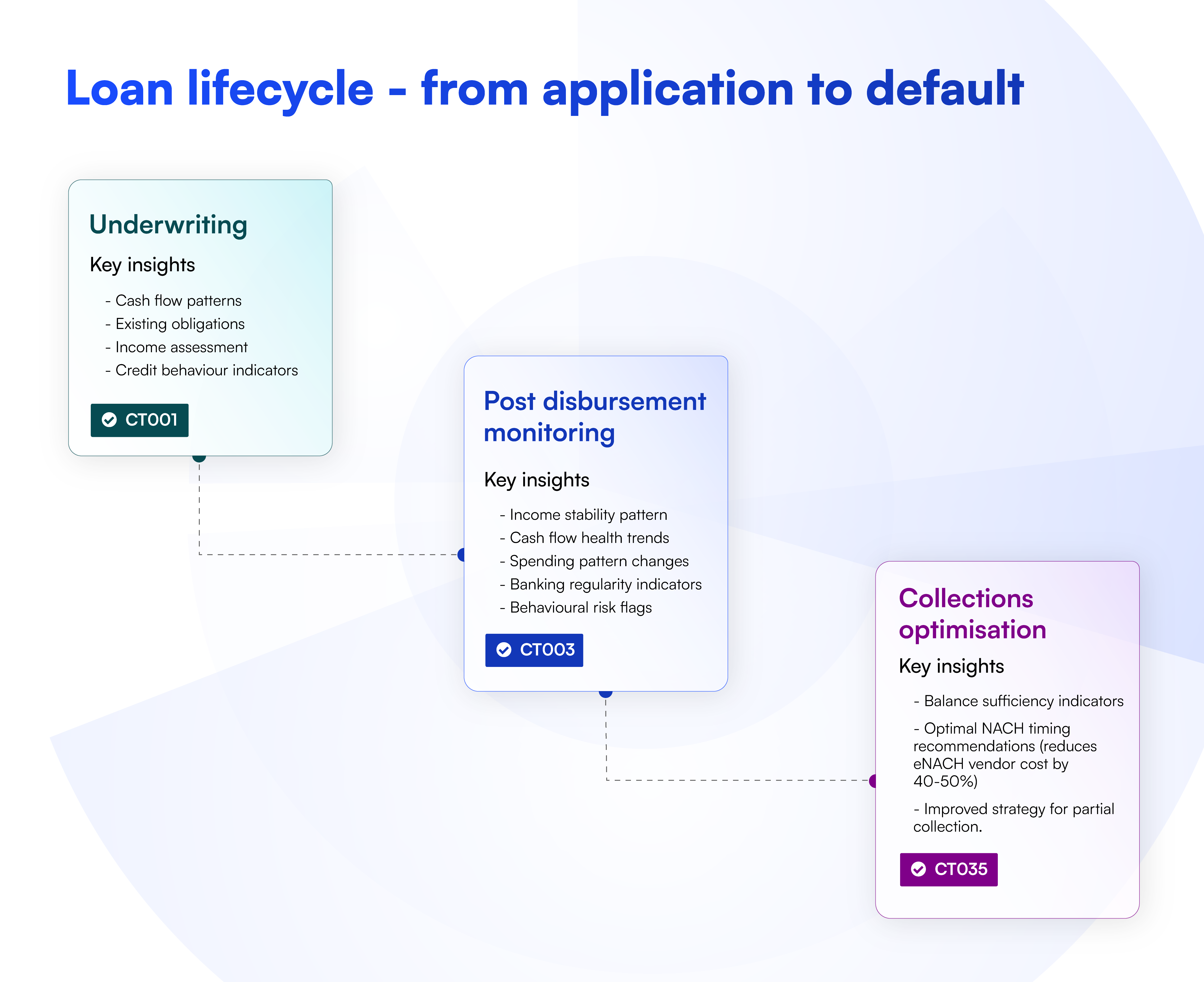

Lenders can typically leverage AA for three main use cases:

Loan underwriting: The well-known use case for credit assessment before loan approval.

Loan monitoring: Continuously tracking borrower financial behaviour post-disbursal to identify risks early and get early warning stress signals.

Collections optimization: Using real-time data for smarter, more empathetic recovery strategies.

How AA enables this in practice

Recurring financial data pulls underpinned by borrower consent allow lenders to:

Monitor cash flows, spending patterns, and income changes in near real-time.

Identify early stress signals that precede defaults.

Tailor collection approaches dynamically based on fresh financial health data.

Predict delinquency with greater accuracy using advanced analytics on AA data.

This continuous data access transforms collections from reactive to predictive, helping reduce write-offs and improve borrower relationships.

The question that arises now is—if AA based data offers so many benefits post disbursal, why hasn’t it been adopted more broadly across these stages?

The challenge: Three barriers to deeper adoption of AA beyond underwriting

Lack of awareness

Many lenders still view AA only as a tool only for loan underwriting, unaware of its potential to streamline monitoring and collection processes. The details and technical flows when it comes to CT003 & CT035 still are lesser known and spoken about in the industry. This brings me to the next point.

Lack of an AA partner with expertise in processing this data

A well formulated monitoring flow demands more than just access—it requires a partner skilled in interpreting AA data, setting up early warning systems, and optimizing recovery strategies. It remains a niche segment from an analytics point of view.

This is exactly where FinBox BankConnect stands out.

Our multi-AA setup delivers some of the highest consent and fetch success rates in the industry, often improving performance by nearly 20–25% compared with relying on a single AA partner.

Post successful fetch, our advanced analytics engine provides tailored insights and built in early warning signals to help you predict delinquency and intervene early.

Lack of customer consent for recurring pulls post disbursal

This third factor is often overlooked yet is the most critical. Without explicit consent, lenders cannot continuously access fresh financial data needed for monitoring and collections.

Fresh consent requests post disbursal can solve for this, but is it really the optimal way of going about it?

Dual consent flow: The practical solution

Luckily, many lenders already have some level of consent for post disbursal monitoring. For those who don’t, implementing a dual consent journey at the first AA interaction can solve the problem efficiently.

This means obtaining borrower’s data sharing consent both for:

The initial underwriting AA data pull.

Recurring data access for ongoing monitoring and collections for the loan tenure.

Embedding these consents upfront prevents future friction and unlocks continuous value from AA data.

It’s time to bridge the gap

If your lending institution hasn’t yet optimized AA for monitoring and collections, now is the time. Taking consent seriously and partnering with AA expertise can transform your entire loan lifecycle.

Don't let this untapped potential slip away.

Start your dual consent journey today and make the most of the Account Aggregator ecosystem.

Learn more about activating these codes and minimise your costs post disbursal.

Contact us to Let’s future-proof your lending business.