The Infinite Loop #21

The Infinite Loop #21: AI-first credit: Slow lenders won't survive

Srijan Nagar

Co-founder, FinBox

·

Two NBFCs came across the same opportunity in early January — credit lines for gig delivery workers, disbursed through a logistics aggregator. I know this because we were talking to both of them. Similar profiles, TAM and even board approvals were secured within weeks.

Same TAM, same unit economics, board approval within weeks of each other.

One was disbursing loans by February. The other was still in UAT in June.

By June, the fast lender had learned something no back-test could have told them: gig workers with six-plus months on the platform and steady UPI inflows default at half the rate the original scorecard assumed.

They’d already widened criteria, grown the book to ₹80 crores, and locked in a six-month exclusivity window with the logistics partner. The second lender launched into a market that had already been shaped by someone else’s data, someone else’s pricing, and someone else’s relationship with the distribution partner.

The second lender’s risk model might have been better. It didn’t matter.

The cost of careful

There’s a belief that runs deep in Indian lending culture — so ingrained that questioning it feels almost irresponsible. The belief is: moving carefully is moving safely.

It sounds right. Lending is a risk business. You don’t rush credit decisions. You validate. You back test. You run a pilot, then a soft launch, then a phased rollout. Caution is professionalism.

Except caution, in practice, looks like a sixteen-week launch cycle. And a sixteen-week launch cycle doesn’t protect you. It just makes you slow enough that someone else captures the opportunity, collects the data, and builds the moat, while you’re being “responsible.”

This is the AI conversation the Indian lending industry isn’t having. Not “should we use AI?” — everyone’s past that.

But: what should AI actually change about how fast we move?

Take a product projected to disburse ₹200 crores in year one, at a net interest margin of 6%. Every week of delay costs roughly ₹23 lakh in NII. A sixteen-week launch cycle bleeds over ₹3.5 crore in foregone interest income before you’ve disbursed a rupee.

That’s the number you can put in a spreadsheet.

The numbers you can’t include: the distribution partner who gave your competitor exclusivity because they were live first. The portfolio performance data your competitor is collecting while you’re in UAT — data that’s actively improving their model while yours sits in a Jupyter notebook. The internal credibility hit when your product team pitched gig lending as a growth lever in January and has just a ₹2 crores book by August, not because the segment didn’t work but because the launch took so long that the window narrowed.

Nobody writes postmortems about these losses. But business takes a hit, and it’s almost always a lost opportunity and thus ensues a game of catching up.

The false dichotomy between speed and accuracy

Speed and accuracy are not trade-offs. Speed is the fastest path to accuracy.

This goes against every instinct a risk professional has, and I understand why. But Upstart, a lending marketplace in the US, made it visible to the entire industry.

When their S-1 dropped, many dismissed their underwriting as reckless. The company was using non-traditional variables, education signals, and employment trajectory to assess borrowers. It felt like astrology dressed up in Python.

Then the default data came in. They were approving 27% more borrowers than traditional models at the same default rate. Not because they started smarter. Because they started sooner, collected real repayment data at scale, and retrained continuously.

The flywheel is simple: launch fast → collect real portfolio data → retrain models on actual outcomes → widen criteria with confidence → grow the book → collect more data. Every rotation makes the model better and the business bigger.

The lender who enters this loop first compounds their advantage with each passing month. The lender who waits for the “right” model never enters the loop at all.

India makes this flywheel more powerful than anywhere else in the world — and most Indian lenders don’t fully appreciate it. The Account Aggregator framework, UPI transaction data, and the emerging OCEN rails give India arguably the richest real-time financial data infrastructure on earth. But that infrastructure is only valuable if you can act on it quickly.

A lender with AI-native systems can ingest AA data, build a cashflow-based underwriting model for a new segment, and go live in days. A lender with traditional infrastructure treats AA as just another data source to integrate and adds four (unnecessary) weeks to the launch cycle for the privilege.

India built the data rails for AI-speed lending. Most Indian lenders are still operating at legacy speed.

Where lenders lose time, business and markets

The time doesn’t die where most people think it does.

Model building is about two to three weeks. It’s the fast part. What kills you is everything that surrounds it.

Data plumbing

Every new product means another bureau integration, another AA connector, another alternate data source, each with its own sandbox, certification process, and testing cycle. At most institutions, this alone eats four to six weeks, and it repeats for every new product because nothing is reusable.

Policy operationalization

The credit policy often lives in a siloed script or a spreadsheet. Translating it into production logic means weeks of back-and-forth with engineering. The clock resets every time she changes a cutoff — which she should be doing regularly, because that’s good risk management. The system punishes her for doing her job well.

UAT and compliance

Testing breaks because a rule changed up stream and nobody flagged it downstream. Compliance wants a full review because the product spec shifted twice. These aren’t failures of diligence. They’re failures of architecture.

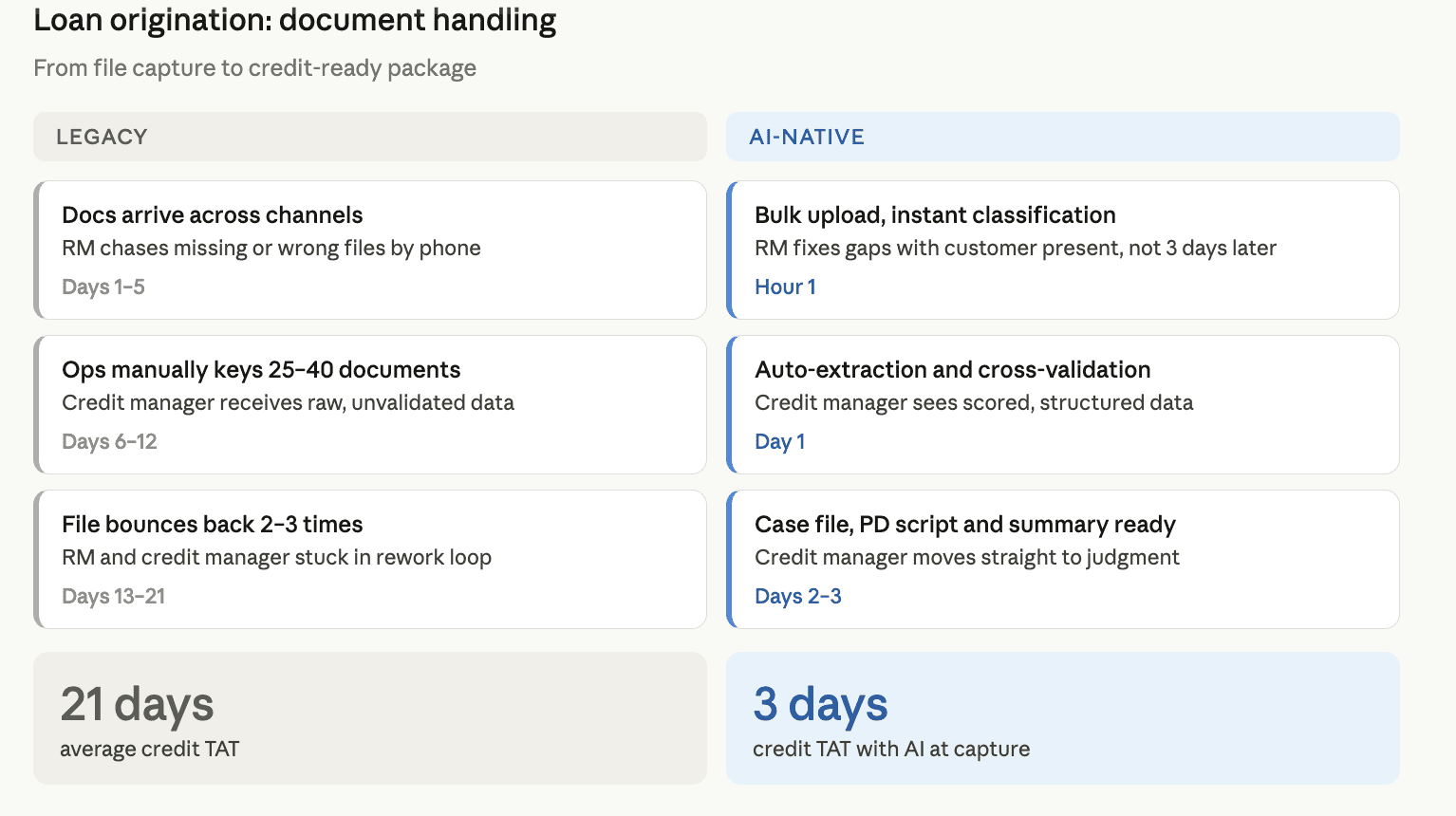

And then there’s document handling. It’s one of the most underestimated drains in the origination cycle, and the one that quietly kills TAT before credit even gets involved.

In a typical file journey, documents arrive across multiple channels. The RM spends days chasing missing or wrong files. Ops manually keys 25–40 documents. The credit manager receives raw, unvalidated data and spends hours assembling it before making a single judgment call. Two to three bounce-back cycles are standard. Twenty-one days average TAT is the result. This is not because anyone is slow, but because the file was never captured cleanly at the start.

Now imagine an AI agent that intercepts the file at the point of capture — classifying documents instantly, flagging missing files before the RM leaves the customer, extracting and cross-validating data automatically, and delivering a structured, scored package directly to credit. The RM stops chasing. The credit manager stops assembling and moves straight to judgment. The twenty-one days becomes three. The rework loop is architecturally eliminated.

An NBFC we work with went from a fourteen-week product launch cycle to eleven days with exactly this solution. Same team. Same risk appetite. Same regulatory environment. The difference was infrastructure, not intelligence.

JPMorgan stumbled into a version of this insight. They deployed a contract intelligence system to review commercial loan agreements, a task that had consumed 360,000 hours of legal time annually. The efficiency headline was obvious. What they didn’t expect: once document review stopped being a constraint, the entire product pipeline moved faster. The AI unclogged the entire system.

MYbank, Ant Group’s lending arm, shows where the flywheel leads if you let it run. Three minutes to apply, one second to decide, zero human intervention. But the part that rarely gets mentioned: that speed didn’t just optimize existing lending. It made micro-loans of ¥5,000 to street vendors economically viable for the first time. That segment wasn’t slow to underwrite; it was impossible to underwrite at human speed. AI didn’t improve the process. It created a market.

The real AI metric in lending that nobody measures

If you’ve invested in AI already — data scientists, scorecards, maybe a deployed model or two — and your honest answer to “how long does it take to launch a new lending product?” is still measured in months, you have an infrastructure problem dressed up as an AI initiative.

The model isn’t the bottleneck. It never was.

There’s a moment in Alice in Wonderland where the Red Queen tells Alice: “It takes all the running you can do, to keep in the same place.”

That’s the situation at most lending institutions today. More models, more data scientists, more POCs — and still not moving forward. Because the pipes can’t convert intelligence into live products fast enough.

A new class of lenders is being built AI-native from the ground up. They’ll never face the sixteen-week problem because they never inherited the plumbing that causes it.

When Jio Financial Services moved from announcement to product at a speed that made the industry blink, it wasn’t because they had better data scientists. It was because they didn’t have thirty years of legacy infrastructure slowing them down.

The question for every incumbent isn’t “are we using AI?” It’s harder than that, and most leadership teams haven’t asked it yet:

How fast can your AI ship?

Somewhere right now, a lender is looking at the same opportunity you are. And their answer to that question is seven days.

Your sixteen-week launch cycle is their window.

I’ll see you next week.

Cheers,

Srijan

Co-founder

FinBox