The Infinite Loop #24

Loan origination is now an AI native workflow

Srijan Nagar

Co-founder

·

There is a pattern in how Indian lending evolved over the last decade.

The sector rebuilt itself piece by piece. Sourcing moved beyond branch walk-ins and onto DSAs, aggregators, and embedded finance partnerships. Data infrastructure took shape around bureau APIs, the Account Aggregator framework, and a steady stream of consented financial signals. Decisioning matured into business rules engines, model frameworks, and increasingly sophisticated scorecards. Disbursal got faster every year as payment rails got better. Collections found its own technology stack, from predictive dialers to digital reminders to restructuring tools.

None of it happened overnight, but the direction was consistent, and most of the leaders reading this lived through that arc and even helped build parts of it.

There is one layer of the stack where the same level of transformation never quite happened: Origination.

The difficulty of loan origination

While significant technological advancements have been made, the inherent problem is that loan origination is not a single workflow. It is a long chain of human-mediated handoffs across capture, onboarding, conversation, validation, and assembly, each requiring something the previous wave of automation couldn't reliably provide. Up until now, existing technology could automate parts of the process, but not the entire loop.

So, the work stayed where it has always been. Relationship managers spend most of their day chasing documents instead of selling. Credit managers assemble files manually before they can underwrite them. Files bounce several times between teams before they reach a decision.

This pattern is invariant across NBFCs and banks of every size, and it scales linearly with volume, which is the structural problem now, because volumes are climbing. NBFCs significantly increased their market share, with loan volume growing to 91.2% (from 86.3% in FY24), and this volume is being absorbed by a layer that has not upgraded proportionally.

Origination has two sides, and both have been stuck

The customer-facing side of origination has digital interfaces, but the interfaces themselves still assume a particular kind of applicant — one who reads English fluently, can easily navigate an unfamiliar app, and understands which document is being asked for at which step. That assumption holds for parts of urban India and breaks for most of the rest of the country.

Over 51% of India's 63 million small businesses operate in Tier 2 and smaller cities, where vernacular language is the default rather than the exception. While the forms were translated, the larger digital journey wasn’t redesigned with those customers in mind.

They drop off mid-form, give up at the upload step, or simply never finish, and the funnel records all of it as abandonment. The underlying cause is rarely creditworthiness. It is that the journey itself asks too much of these customers: to navigate an unfamiliar app, decode banking terminology, fill redundant fields, and do all of it in a language that often isn't their first.

The RM and credit side has had its own version of the problem. The technology that arrived in this part of the workflow could extract data from documents but could not reason across them — could not look at an ITR, bank statements, and a GST return and decide which discrepancies are concerning. That reasoning stayed with the credit manager, which meant the credit manager's day still began with an hour or more of pre-judgment work: locating documents, reading them in sequence, building context, identifying gaps, drafting the financial summary, preparing the PD script.

None of this is credit judgment, but all of it has been a credit manager's job because there was no system layer capable of taking it off their plate.

What kept origination stuck

Many layers of the stack could be built through rules, APIs, and structured data, because the work in those layers was already legible to machines. A payment is a payment. A rule fires or it doesn't. A bureau pull returns a number. The shape of the work matched the shape of the available technology, and once the integration work was done, the layer could scale on its own.

Origination has never been like that. The work has always required reading unstructured content, interpreting human responses, weighing documents against each other, and routing the file based on judgment calls that resist being hard-coded. The previous wave of tools could handle pieces of this — capture here, extraction there, a workflow engine somewhere in the middle — but no single system could run the loop end to end, because doing so required language understanding and contextual reasoning that simply hadn't matured yet in any production-grade way.

That has changed in the last two years. Language models became capable enough to read unstructured and vernacular documents and understand them, not just transcribe them. Agentic architectures became reliable enough to close their own loops: capture, validate, observe what happened, retry where needed, and escalate to a human when judgment is required.

The combination matters more than either piece alone. The agent runs the workflow. The human runs the decision.

For the first time, the shape of the technology matches the shape of the work in this layer.

Introducing Atlas

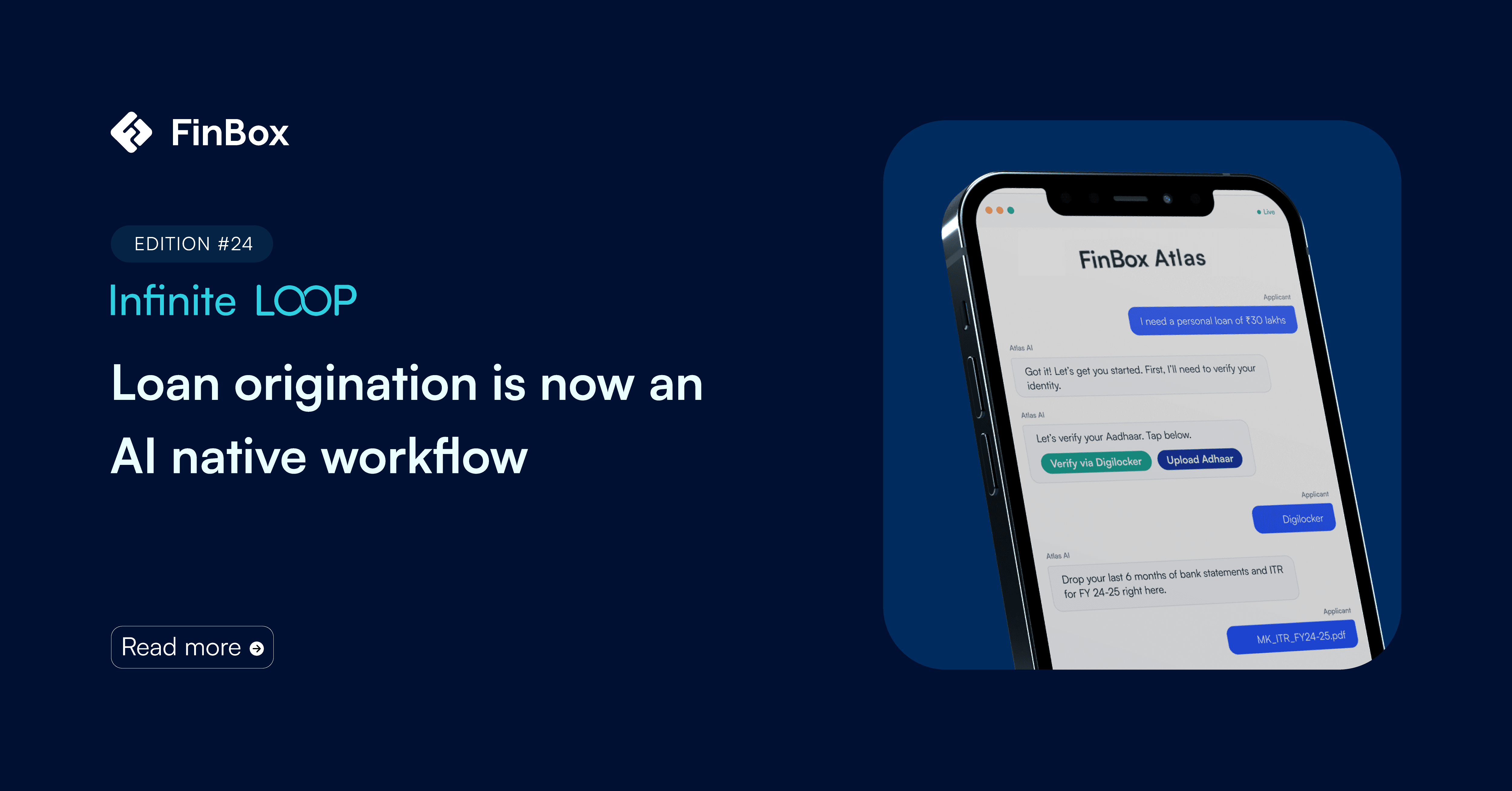

This is the context in which we built Atlas, an agentic AI suite for the origination layer that launches today.

Atlas Flow handles the customer side, a conversational onboarding agent that meets applicants in their language, accepts vernacular documents and voice, and structures the interaction into a clean file.

Atlas Origin handles the RM and credit side, an autonomous agent that classifies documents at the point of capture, validates them against policy, cross-references declared and documentary data, and delivers a decision-ready file with a drafted financial summary and PD script.

Flow's output is Origin's input, and the file moves through the layer end-to-end with the agentic loop doing the assembly and the human owning the judgment call.

What changes once this layer is redesigned

When a layer of the stack gets rebuilt, the operating math of everything around it changes too. When decisioning got rebuilt, credit policy itself moved closer to the data. The same happened with disbursal; once payment became instant, customer expectations of speed reset across the industry.

Origination will do the same thing. Once the assembly work stops being a human bottleneck, RMs will spend their days selling instead of chasing. Credit managers will spend their days judging instead of assembling. Customers will stop being filtered out by a journey that wasn't built for them. The cost of producing a decision-ready file will fall, and the volume each team can handle will rise. Early pilots with our partners are already showing these patterns play out.

If you want to follow along, we are documenting the build as it happens: what we are trusting the agent with, where things break, and what we are learning at withfinbox.ai.

Until next time,

Srijan

Co-founder

FinBox